Could first-class, long-haul flights and airport lounges be next at Southwest Airlines?After all the changes to the airline’s long-standing business model in recent months, including bag fees, assigned seats and bigloyalty program shake-ups, the company’s top executives seemingly aren’t ruling anything out.

“We aren’t stopping here,” Southwest CEO Bob Jordan acknowledged, speaking Thursday at an industry conference in New York.

By next year, Jordan said, Southwest plans to unveil itsnextround of long-term plans — the next chapter, if you will, in the evolution that so far has ushered in assigned seats, $35 bags and, for the first time at the airline, basic economy.

What else could be on the horizon?

“There’s no reveal today,” Jordan cautioned. But he also posed some “hypothetical” examples of what the airline might consider.

“For many of our folks that love Southwest, we can’t do things — we can’t provide products — that you want. Like a first class. We can’t get you to long-haul international destinations. If a lounge is important to you, we don’t have a lounge,” Jordan said while speaking at the Bernstein Strategic Decisions Conference.

“I’m not predicting any of those things,” he reiterated while making clear that “we will continue to pursue the consumer.”

And consumer demand for a lounge in some key Southwest cities, Jordan noted, is “super high.”

He also acknowledged that rethinking Southwest’s international strategy (and pushing beyond its short-haul flights to places like Mexico and the Caribbean),“could require that you think about a different aircraft.” The carrier currently has a fleet of entirely narrow-body Boeing 737s.

“What I’m promising you,” Jordan said, “…is that we will never lack a ‘where we head five years from now’ strategy.”

Evolving, but increasingly less different

Again, none of this is officially “on the table,” so to speak.

In the wake of the coronavirus pandemic, it’s carriers like Delta Air Lines and United Airlines that have soared to the U.S. airline industry’s highest profits, propelled by their robust international networks,premium seatsand lucrative credit card portfolios.

Southwest, meanwhile, hasn’t maintained its historically high margins — a driving force behind the shift the airline has gone through in recent months.

“The old model wasn’t working and so now we’ve pivoted,” Southwest Chief Operating Officer Andrew Watterson acknowledged on the company’s earnings call last month.

Competing with premium airlines

Yet there’s a stark reality in Southwest’s pivot: Yes, it will soon have more premium options in its extra-legroom rows. Yes, it’ll offer “upgrades” to A-List elite members and certainRapid Rewards credit card holders.

But even as Southwest matches Delta, United, American Airlines and Alaska Airlines in charging customers add-on fees for bags (and eventually seats, on some fares), it still won’t have the first-class seats and lounges those carriers offer. Even Frontier Airlines isadding bona fide premium seats, and JetBlue has announcedloungesand adomestic first-class productto complement its long-haul Mint suites.

That contrast, as Brian Sumers of The Airline Observerwrote in March, arguably puts Southwest at a disadvantage as it begins to look more like its competitors in other areas.

And it’s a contrast I posed to Tony Roach, executive vice president of customer and brand, during a recent interview just a few weeks ago.

“There’s nothing to announce on lounges or first class,” Roach cautioned then, with a similar tone to what Jordan offered during his remarks this week.

“But you can almost assume that, if this is a product offering that our customers ultimately are going to want and demand from Southwest Airlines, we’ve demonstrated that we’ve got to continue to evolve, serve more of those needs,” he added. “We continue to look toward long term, the future of Southwest, which we, again, continue to offer more things that’s going to give people more reason to choose Southwest.”

SEAN CUDAHY/THE POINTS GUY

Planning for the future

Whether customers would continue to choose a vastly different-looking Southwest was the subject of plenty of speculation this spring.

So far, so good, executives claimed last month, noting the carrier had not, as of yet, shed passengers to competitors.

“After announcing these changes, we saw no evidence of bookaway,” Jordan told analysts in April.

But maintaining that momentum, he suggested this week, could require Southwest to continue evolving.

It’s conceivable that quest could lead the airline to more of the features — and flights — that its competitors (and their customers) have flocked to in recent years.

SEAN CUDAHY/THE POINTS GUY

“Because we can’t offer certain products and get you to certain destinations, even customers that love Southwest, we force you to fly on somebody else. And we then force you to carry somebody else’s cobrand [credit] card,” Jordan saidThursday, committing to “study” that gap over the coming months.

“I would think about that,” he added, “… as a 2026 question.”

It carries a high $595 annual fee, but there are several easy ways to get excellent value from both the card and the AAdvantage program. And currently, the card is offering its highest-ever welcome bonus.

Here are six reasons why the Citi / AAdvantage Executive World Elite Mastercard could be a smart addition to your wallet.

Welcome offer

The first reason is straightforward and relatively obvious: the valuable welcome bonus.

This also includes two guests or your immediate family (defined as a spouse or domestic partner plus dependent children under the age of 18).

ZACH GRIFF/THE POINTS GUY

Primary cardholders also receive access to Alaska Airlines lounges when departing or arriving on a flight operated by Alaska or American Airlines.

It’s also worth pointing out that the annual fee on the card ($595) is actually less than purchasing a lounge membership outright — an individual Admirals Club membership ordinarily costs between $750 and $850, depending on your status level with American, with a household membership costing up to $1,650.

Authorized user access to Admirals Clubs

Authorized users on the Citi / AAdvantage Executive World Elite Mastercard get access privileges to American Airlines Admirals Club lounges, just like the primary cardholder. This can offer significant value to friends or family members who travel even a few times a year.

The total cost for up to three authorized users is $175, and $175 for each authorized user thereafter.

Sure, you can bring in two guests or your immediate family as the primary cardholder, but what if your partner, parent or close friend is traveling alone? Adding them as an authorized user will get them into an Admirals Club, even when they’re not traveling with you.

There are many ways to avoid fees for checked baggage when traveling, and cobranded airline credit cards are a great way to accomplish this goal. With the Citi / AAdvantage Executive World Elite Mastercard, you and up to eight traveling companions on the same reservation can check a bag for free on all American-operated domestic flights.

This saves each passenger at least $80 per round-trip flight within the U.S., Puerto Rico and the U.S. Virgin Islands, so the savings can really add up.

This perk applies even if you don’t use the card to book your flight. This is especially beneficial if you want to use another credit card that provides elevated rewards on airfare purchases or are required to book a ticket using a company card.

Global Entry is a great way to expedite your reentry into the U.S. after international travel. And I’d strongly encourage you to go for the gold with Global Entry, as PreCheck comes included with a Global Entry membership.

DAVID PAUL MORRIS/BLOOMBERG/ GETTY IMAGES

You can also use this credit for someone else — not just yourself or an authorized user. Citi will simply look for an applicable charge on your statement and will credit you the membership fee, even if the card was used for a friend’s or family member’s application.

Access to Admirals Club privileges (which extends to any authorized users you add), perks when flying American and Global Entry credit make the card a terrific value proposition, even with the steep annual fee.

As an Amex Platinum cardmember, you earn 5 points per dollar on flights booked directly with airlines or American Express Travel® (on up to $500,000 of these purchases per calendar year, then 1 point per dollar) and 5 points per dollar on prepaid hotels and flights booked through American Express Travel®.

In addition, cardmembers receive a wide array of statement credits, hotel and car rental elite status, travel protections and special offers through Amex Offers.

With so many benefits to keep track of, some Amex Platinum cardmembers feel like their card acts more like a coupon book than a premium travel card.

If you are unsure whether to keep your Amex Platinum, consider switching to one of these 9 rewards credit cards.

The Capital One Venture X Rewards Credit Card is a worthy competitor in the luxury rewards card space. The card includes an annual $300 travel credit when booked through Capital One Travel, a 10,000-mile anniversary bonus, a Priority Pass membership, access to Capital One Lounges and a credit of up to $120 for Global Entry or TSA PreCheck.

THE POINTS GUY

It earns 10 miles per dollar spent on hotels and rental cars and 5 miles per dollar spent on flights and vacation rentals when booking through Capital One Travel, as well as 2 miles per dollar spent on all other purchases. Plus, as a new cardmember, you can earn a welcome bonus of 75,000 miles after spending $4,000 on purchases within the first three months of account opening.

All miles can be used to book travel and even cover eligible travel purchases, or you can transfer them to one of Capital One’s 15-plus airline and hotel partners. The card does have an annual fee of $395, but authorized users (a number of which can be added at no additional cost) can enjoy many of the card’s benefits.

$395 isn’t a small amount, but it’s significantly less than what an Amex Platinum cardmember pays each year.

With this card, you’ll receive an annual $300 travel credit, up to a $120 credit for Global Entry, TSA PreCheck or Nexus, access to every Chase Sapphire Lounge, a Priority Pass membership, access to The Edit (Chase’s rebranded luxury hotel program), primary rental car coverage and travel and shopping purchase protections.

THE POINTS GUY

Additionally, you’ll earn 3 points per dollar spent on travel and dining (including eligible takeout and delivery services), 5 points per dollar spent on flights booked through Chase Travel, 10 points per dollar spent on hotels and car rentals booked through Chase Travel and 10 points per dollar spent on Chase Dining purchases. All other purchases earn 1 point per dollar.

Note that you won’t earn bonus points on travel until after the first $300 is spent on travel annually.

You can transfer points to 14 airline and hotel partners or use them to book travel and cover purchases through statement credits. You’ll have to pay a $550 annual fee, but that means you’ll save $145 each year compared to paying for an Amex Platinum. Sapphire Reserve authorized users cost $75 each.

New cardholders can earn 60,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

As a cardmember of the Amex Platinum and the Sapphire Reserve, TPG credit cards writer Danyal Ahmed consistently gets better value out of his Sapphire Reserve thanks to its amazing earning rates and flexible travel credit.

While this card doesn’t include lounge access and other premium benefits, it does come with primary rental car insurance, a $50 annual hotel statement credit on bookings made through Chase Travel and travel and shopping purchase protections. Additionally, you’ll receive a 10% points bonus on all purchases at the end of every year.

THE POINTS GUY

Travel booked through Chase Travel earns 5 points per dollar. You’ll also earn 3 points per dollar spent on dining (including eligible takeout and delivery services), online grocery purchases (excluding Target, Walmart and wholesale clubs) and select streaming services, 2 points per dollar spent on all other travel and 1 point per dollar spent on everything else.

This card’s annual fee is a reasonable $95. New applicants can earn 60,000 bonus points after spending $5,000 on purchases in the first three months from account opening

Every year, you’ll receive a $100 credit toward a single hotel stay of $500 or more (excluding taxes and fees) that’s booked through CitiTravel.com. This benefit alone covers the $95 annual fee.

THE POINTS GUY

You’ll earn 10 points per dollar on hotels, car rentals and attractions booked on CitiTravel.com, 3 points per dollar spent at restaurants, supermarkets, gas stations and electric vehicle charging stations, as well as 3 points per dollar spent on air travel and other hotel reservations. All other purchases earn 1 point per dollar.

New cardholders will earn 60,000 bonus points after spending $4,000 on purchases in the first three months of account opening.

If you want to keep earning Membership Rewards points, the American Express® Gold Card may be the right card for you. With the Amex Gold, you’ll earn 4 points per dollar dining at restaurants worldwide (on up to $50,000 in purchases per calendar year; then 1 point per dollar), 4 points per dollar on groceries at U.S. supermarkets (on up to $25,000 in purchases per calendar year; then 1 point per dollar), 3 points per dollar on flights booked directly with the airline or with amextravel.com and 2 points per dollar on prepaid hotels booked with amextravel.com and 1 point per dollar on other eligible purchases.

THE POINTS GUY

Amex Gold cardmembers also receive up to $120 in Uber Cash per calendar year (up to $10 a month), up to $120 in dining statement credits (up to $10 per month) per calendar year, up to $100 in statement credits with U.S. Resy restaurants (up to $50 in statement credits semi-annually) per calendar year and up to $84 in monthly statement credits (up to $7 per month in statement credits) per calendar year with U.S. Dunkin’ Donuts locations. Enrollment is required for select benefits; terms apply.

When fully utilized, these credits provide enough value to more than cover the card’s $325 annual fee (see rates and fees). Uber Cash will only be deposited into one Uber account when you add an Amex Card as a payment method and pay with any eligible Amex card.

Plus, cardmembers have access to the same Hotel Collection* benefits as those with the Amex Platinum. Enrollment is required.

New applicants for the Amex Gold can earn 60,000 bonus points after spending $6,000 on purchases in the first six months of cardmembership.

The Bank of America® Premium Rewards® credit card is a great option for travelers who are loyal to Bank of America. It earns 2 points per dollar spent on travel and dining purchases, plus 1.5 points per dollar spent on everything else.

Cardholders who are also a member of the Bank of America Preferred Rewards® program can earn up to a 75% bonus on all of their rewards, depending on the size of their account balances. That translates to up to 3.5 points per dollar spent on travel and up to 2.63 points per dollar spent on everything else.

THE POINTS GUY

While Bank of America doesn’t have any transfer partners, you can redeem your points for cash back, as a statement credit, for gift cards and for travel purchases through the Bank of America Travel Center without blackout dates.

You’ll also receive up to $100 for Global Entry or TSA PreCheck application fees every four years and up to $100 in airline incidental fee statement credits each year, the latter of which offsets the card’s $95 annual fee.

New cardholders can earn 60,000 online bonus points after making $4,000 in purchases within the first 90 days of account opening.

Hilton loyalists love the Hilton Honors American Express Aspire Card because it automatically grants Hilton Diamond elite status and offers an array of other benefits. Cardmembers receive a variety of statement credits, tailored toward both general travel and Hilton stays.

The card also includes an annual free night reward. Additional free night rewards can be earned when you spend $30,000 and $60,000 in a calendar year. These benefits easily outweigh this card’s $550 annual fee. Enrollment is required for select benefits; terms apply.

The information for the Hilton Aspire Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

THE POINTS GUY

You’ll earn 14 points per dollar spent on eligible purchases at hotels and resorts in the Hilton portfolio, 7 points per dollar spent on flights booked directly with the airline or American Express Travel and car rentals booked with select car rental companies, 7 points per dollar spent on dining at U.S. restaurants (including takeout and delivery) and 3 points per dollar spent on other eligible purchases.

New cardmembers can earn 150,000 bonus points after spending $6,000 on purchases in the first six months of card membership.

The Marriott Bonvoy Brilliant® American Express® Card is the premier card for Marriott Bonvoy members. It includes up to $300 in annual statement credits per calendar year (up to $25 per month) on eligible dining purchases made with the card at restaurants worldwide, plus automatic Platinum Elite status and a free night award every year after your renewal month (worth up to 85,000 points). Certain hotels have resort fees.

You’ll also receive up to $100 in property credits when you book at least two nights at a Ritz-Carlton or St. Regis. If that wasn’t enough, cardmembers get a Priority Pass membership and up to $120 for Global Entry or TSA PreCheck. Enrollment is required; terms apply.

THE POINTS GUY

With this card, you’ll earn 6 points per dollar spent on eligible purchases at hotels participating in the Marriott Bonvoy program, 3 points per dollar spent on dining at restaurants worldwide and on flights booked directly with the airline, and 2 points per dollar spent on everything else.

An annual fee of $650 (see rates and fees) applies, but the yearly statement credits, automatic elite status and free night certificate are worth at least that much. Plus, it’s still more affordable than the Amex Platinum, even if not by much.

New cardmembers can earn 100,000 bonus points after spending $6,000 in purchases within the first six months of card membership and an extra 50,000 bonus points after spending an additional $2,000 in purchases within the first six months.

If Delta is your favorite Amex transfer partner, then the Delta SkyMiles® Reserve American Express Card should be one of your frontrunners. As a cardmember, you’ll earn 3 miles per dollar spent on eligible Delta purchases and 1 mile per dollar spent on other eligible purchases.

Plus, new applicants can earn 70,000 miles after spending $5,000 in the first six months of card membership. This card frequently offers elevated welcome offers, so keep an eye out for one.

THE POINTS GUY

Although this card has a steep $650 annual fee (see rates and fees), cardmembers receive all kinds of benefits, including access to Delta Sky Club lounges when traveling on a same-day, Delta-marketed or Delta-operated flight. Access is limited to 15 free annual visits, with unlimited annual visits after spending $75,000 in a calendar year.

Plus, those without elite status will be added to the upgrade list after Medallion members when flying with Delta, while those with status will receive priority upgrades over other Medallion members. You’ll also receive various lifestyle and travel statement credits to help offset the annual fee.

It’s also possible to accelerate earning elite status with this card, as you’ll earn one Medallion Qualification Dollar for each $10 spent with the card in a calendar year. You’ll also earn a head start of 2,500 MQDs each Medallion Qualification Year to get closer to status with the card.

While the Amex Platinum still holds value for many cardmembers, others may feel inclined to get rid of the card in favor of another on the market. Fortunately, there are several great alternatives to consider.

Each card comes with its own pluses and minuses, though in many cases, each offers similar (if not better) benefits as the Amex Platinum for a lower annual cost. Regardless of where your loyalties lie, there’s a card that will suit your spending habits and travel goals.

For rates and fees of the Amex Platinum Card, click here. For rates and fees of the Amex Gold Card, click here. For rates and fees of the Marriott Bonvoy Brilliant Amex, click here. For rates and fees of the Amex Delta Reserve card, click here.

Editor’s note: This is a recurring post, regularly updated with new information and offers.

If you have upcoming travel to any of IHG’s brands — including Holiday Inn, Crowne Plaza, Kimpton, InterContinental and Hotel Indigo — an IHG cobranded card can save you hundreds of dollars year after year.

Now is the perfect time to apply, as for a limited time, the two personal cards have the highest welcome offers we’ve seen in at least eight months. IHG currently offers two personal and one business credit card.

Let’s examine these welcome offers and determine which IHG One Rewards card is best for you.

Welcome bonus: For a limited time, earn five free nights (up to 60,000 points per night) after spending $5,000 in the first three months from account opening. This offer ends July 23.

If you max out each night at 60,000 points, the bonus could be worth up to 300,000 points. According to TPG’s May 2025 valuations, that makes it worth up to $1,500.

This matches the card’s highestwelcome offer, which has only been offered once in the card’s offer history (in September last year). However, it does require an additional $1,000 in minimum spending ($5,000 instead of $4,000). Despite this higher minimum spending requirement, now is a great time to apply if you’ve been eyeing this card.

Annual fee: $99

Earning rates: Cardholders earn:

10 points per dollar spent on IHG stays

5 points per dollar spent on all other travel

5 points per dollar spent on dining (including takeout and eligible delivery services) and gas stations

3 points per dollar spent on all other eligible purchases

Why we like it: This card comes with a free night worth up to 40,000 points on each account anniversary and the option to top off your reward to redeem it for a more valuable night.

Other important perks include complimentary IHG Platinum Elite status (with a pathway to Diamond), up to $50 of United TravelBank cash per calendar year, reimbursement for your application fee to Global Entry, TSA PreCheck or Nexus every four years and more — all for a $99 annual fee.

Factoring in the card’s fourth-night-free perk (when you use points to pay for three nights and get the fourth as a bonus) is an important consideration when thinking about the potential value you can get out of it. Reward nights start at just 10,000 points apiece, ranging from practical options in the U.S. to lodgings abroad in Berlin, Brazil and beyond.

If you only stay with IHG once or twice each year, the IHG One Rewards Traveler Credit Card may make more sense for you than IHG’s premium option.

THE POINTS GUY

Welcome bonus: For a limited time, earn 120,000 bonus points after spending $2,000 in the first three months from account opening. This offer ends July 23.

According to TPG’s May 2025 valuations, this bonus is worth $600.

This matches the highest ever offer we’ve seen on this card, which was last offered over two years ago, making now an excellent time to apply.

Annual fee: $0

Earning rates: Cardholders earn:

5 points per dollar spent on IHG stays

3 points per dollar spent on utilities, dining (including takeout and eligible delivery services), select streaming services and gas stations

2 points per dollar spent on all other eligible purchases

Why we like it: This card offers complimentary Silver Elite status and the ability to get a fourth night free on bookings where you pay with points. Plus, the current welcome bonus is solid for a card with no upfront, annual cost.

Welcome bonus: Earn 140,000 points after spending $4,000 in the first three months from account opening.

TPG’s May 2025 valuations peg those 140,000 IHG points up to $700.

This is the standard offer on the card. The highest welcome bonus we’ve seen offered was 175,000 bonus points a little over a year ago (no longer available). So, you might be better holding off on applying until there is a higher bonus.

Annual fee: $99

Earnings rate: Cardholders earn:

10 points per dollar spent on IHG stays

5 points per dollar spent on dining, gas, office supply stores, search engine advertising, social media and travel

3 points per dollar spent on all other eligible purchases

Why we like it: The IHG One Rewards Premier Business Credit Card mimics many of the same great perks of the consumer IHG One Rewards Premier Credit Card.

For instance, the annual free night award (worth up to 40,000 points) can be topped off with an unlimited number of points, and you’ll also enjoy elite perks thanks to automatic IHG Platinum Elite status.

IHG Premier Business cardholders can also earn an additional free night award worth up to 40,000 points (that can also be topped off with additional points) after spending $60,000 each calendar year.

Other benefits include reimbursement for your application fee to Global Entry, TSA PreCheck or Nexus once every four years, a fourth night free on award stays and up to $50 of United TravelBank credit each calendar year.

Reasons to get an IHG One Rewards card beyond the bonus

Earning a chunk of bonus points for adding a new card to your wallet is very enticing, but these three cards offer a lot of potential value beyond that initial haul of points.

Elite status

Every IHG One Rewards card offers complimentary elite status.

You should be able to recoup the $99 annual fee on the consumer or business version of the Premier card if you spend more than a few nights a year at IHG properties. The benefits Platinum Elite status provides include early check-in and late checkout (subject to availability) and 60% bonus points on IHG stays.

Fourth-night-reward benefit

All IHG One Rewards cardholders automatically get a fourth consecutive night reward. In short, the fourth night is complimentary when you redeem points for stays of four or more.

IHG HOTELS & RESORTS

This benefit’s value depends on your travel style. This isn’t very useful for travelers who only book short hotel stays, but it can be incredibly worthwhile for travelers who stay long enough to utilize this perk. And this benefit has no cap on how many points you can save.

TPG’s May 2025 valuations peg IHG points at 0.5 cents each. Thus, a single fourth-night reward stay at a 20,000-point property saves you $100 worth of IHG points.

The IHG One Rewards cards help you rack up points fast, thanks to their bonus categories — including gas, which can be an expensive recurring purchase for many households.

But it gets better than that. Since the IHG One Rewards Premier and the IHG One Rewards Premier Business grant you complimentary Platinum Elite status, you’ll also earn a 60% points bonus on IHG hotel stays.

IHG One Rewards base members earn 10 points per dollar spent at most properties, so the 60% elite bonus provides 16 points per dollar at IHG properties. Add that to the 10 points per dollar you earn with either card and you’ll get 26 points total per dollar spent on these cards on IHG hotel stays, equating to a 13% return (based on TPG’s May 2025 valuations).

Buying points discount

Finally, if you need to top off your IHG points balance, you can get a 20% discount when you buy points with your card. Combined with the ability to top off free night certificates, this perk could be handy if you’re looking to save up your awards for aspirational stays.

You can have multiple IHG credit cards, but know that the IHG One Rewards cards, like all other Chase cards, are subject to Chase’s 5/24 rule. This means if you’ve opened five or more personal credit card accounts across all banks in the last 24 months, Chase is unlikely to approve you.

Note that you also aren’t eligible if any of these exclusions apply to you:

For personal cards: If you currently have a personal IHG One Rewards credit card (which includes the legacy IHG One Rewards Select Credit Card (that’s no longer available to new applicants) or if you received a new cardholder bonus on any personal IHG credit card in the past 24 months.

For the IHG Business card: You received a new cardmember bonus on this card in the last 24 months.

The information for the IHG One Rewards Select Credit Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

American Airlines has finally gone live with one of the biggest time-savers that exists today at Transportation Security Administration checkpoints.

The carrier on Thursday launched TSA PreCheck Touchless ID at four major airports, including two of its busy East Coast hubs.

As part of the new partnership, TSA PreCheck members flying with American will be able to fly through checkpoints without showing their physical ID or boarding pass.

The program just launched for American flyers at its Ronald Reagan Washington National Airport (DCA) and LaGuardia Airport (LGA) hubs, along with Hartsfield-Jackson Atlanta International Airport (ATL) and Salt Lake City International Airport (SLC).

TSA checkpoint at New York’s LaGuardia Airport (LGA) Terminal B. SEAN CUDAHY/THE POINTS GUY

Travelers using TSA Touchless ID will get their photo taken once they approach the agent, and they won’t need to pull out a driver’s license or passport. To verify the traveler’s identity, the system will quickly compare that image to others the government has on file, like the one on a passport or in a trusted traveler program like Global Entry.

American had announced last fall it would join in on the TSA’s faster, high-tech screening process. TPG’s Clint Henderson noted in October that this biometric setup has, at times, proven faster than paid services like Clearat airports where competing airlines (such as Delta Air Lines and United Airlines) had already partnered with the TSA.

CLINT HENDERSON/THE POINTS GUY

American hopes to expand Touchless ID to more airports across its network, with a particular focus on its biggest hubs.

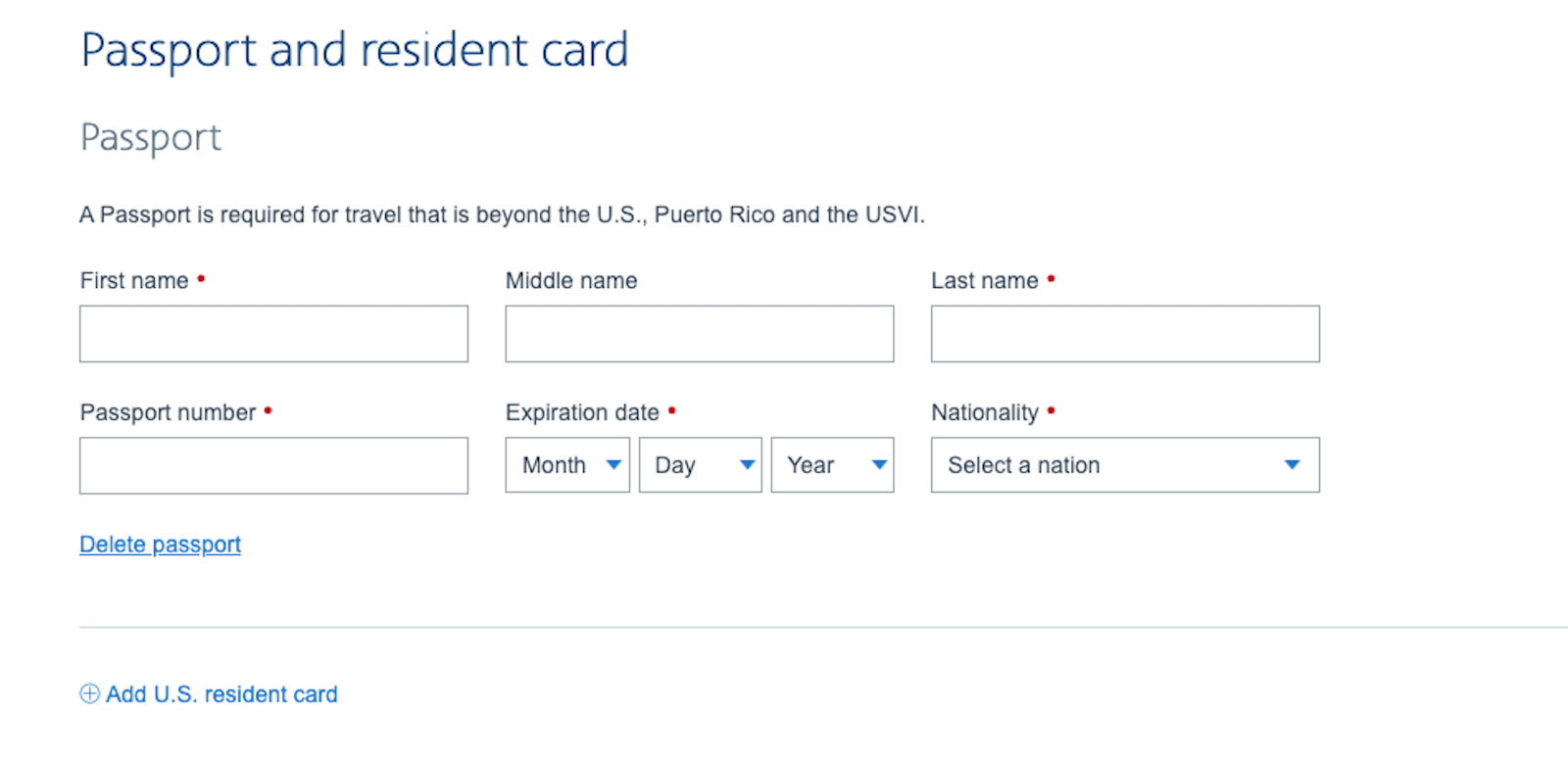

Travelers who want to opt into the faster security process must update their AAdvantage profile on the American website.

It took me all of two minutes.

You’ll want to log in and go to the “information and password” section of your profile.

There, you’ll need to add your passport number and expiration date.

AMERICAN AIRLINES

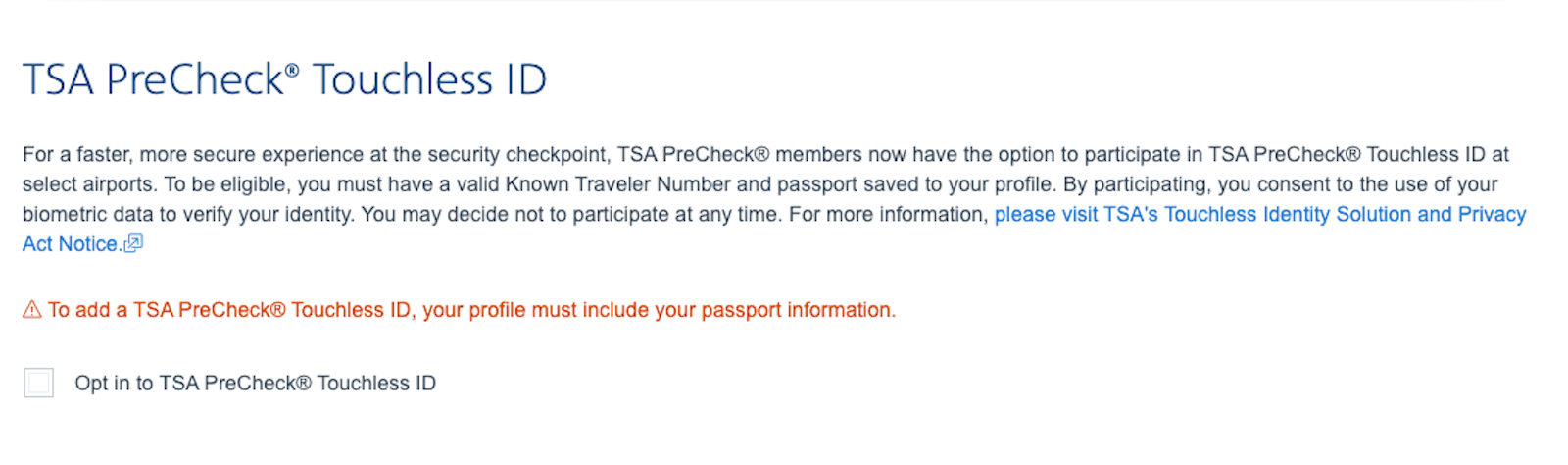

Then, click the box to opt in to TSA Touchless ID.

AMERICAN AIRLINES

It’s optional, so travelers who don’t want to opt into the touchless program can stick with showing the agent their identification each time they fly.

Travelers will need to renew their enrollment in the program each year.

It’s free, aside from the existing membership fee required to access the TSA PreCheck lanes. For new members, TSA PreCheck starts at $78 for a five-year membership.

Global Entry, which offers both PreCheck access and an expedited trip through U.S. Customs and Border Protection passport control, costs $120.

I’ve been involved in the world of points and miles for over a decade, and not once have I applied for a cobranded hotel credit card. Although this might come as a surprise to most people, my travel habits just haven’t required me to need one.

Although I travel around 100,000 aeronautical miles a year, I don’t stick to a single hotel brand and have been very open with the brands I choose to stay at. When I book a hotel, I focus on price, location and the uniqueness of the property. This makes me open to all brands, but I tend to end up at ones without a loyalty program.

Here are my top reasons why I haven’t needed a cobranded hotel credit card, and how I’ve managed to make it work with the current credit cards in my wallet.

I’m not loyal to 1 brand

When most people think of hotel brands, they tend to focus on the three major ones: Marriott, Hilton and Hyatt. These brands have several types of hotels in their portfolios, from budget to extended-stay to high-end properties.

Mandarin Oriental Hyde Park, London. DANYAL AHMED/THE POINTS GUY

When booking properties for domestic or international trips, I consider various factors, including price, ratings, location and amenities.

Occasionally, I’ll end up at a Marriott property since it has the largest hotel portfolio. But 75% of the time, Marriott hotels are not in my location of choice (or at the right price point).

A big reason why I don’t see a need for a cobranded hotel credit card is that the majority of the properties I stay at have no loyalty ecosystem. These properties include Four Seasons, Mandarin Oriental, Rosewood, Aman and One&Only.

Quite frankly, I travel specifically to certain destinations because the brands mentioned above tend to have unique and luxurious properties. These properties provide a level of service, amenities, personalization and quality that is hard to beat, even when staying at top-tier properties with brands that offer cobranded credit cards.

Four Seasons Resort Seychelles. DANYAL AHMED/THE POINTS GUY

For example, Four Seasons has some of the comfiest mattresses in the industry, so much so that it even sells them. I travel with my family often, and whenever these brands see a small child on the reservation, they almost always provide amenities and special gifts.

Because the hotel brand I stay at varies, it’s more beneficial for me to use my Chase Sapphire Reserve® (see rates and fees) to earn 3 points per dollar spent on purchases coded as travel, including hotels. I’ll later redeem those points for airfare by transferring to one of Chase’s 11 airline partners.

Best of all, the Sapphire Reserve offers a flexible $300 annual travel credit to apply to anything that codes as travel, according to Chase, so this credit can automatically be applied to any hotel purchase. In the past, I’ve called hotels after my $300 credit has reset and asked the property to charge my Sapphire Reserve $300, instantly using my credit.

Marriott consistently runs a double-night promotion from February to April every year, where each paid night earns you a bonus elite night credit. In order to earn Marriott Bonvoy® Platinum Elite status, you need to stay 50 nights within a calendar year. During the double-night promotion, I stay about 15 to 20 nights, which earns me between 30 to 40 nights right off the bat.

But like airline frequent flyer programs, hotel loyalty programs are subject to devaluations. Earlier this year, TPG calculated a drop in value for Marriott Bonvoy points toward stays across various properties worldwide.

By opening a cobranded hotel credit card, I am investing in the program for the long run. I am tying myself to the hotel program by staying almost exclusively with that brand and using the brand’s card for purchases that will give me bonus points.

Phulay Bay, a Ritz-Carlton Reserve. DANYAL AHMED/THE POINTS GUY

The points earned on a cobranded hotel credit cardare also valued quite low. For example, based on TPG’s May 2025 valuations, Marriott Bonvoy points are worth 0.7 cents each. On the flip side, transferable points from programs like Chase Ultimate Rewards and American Express Membership Rewards are worth 2.05 and 2 cents apiece, respectively.

When I first started collecting points and miles a decade ago, Marriott had a fixed award chart that made it easy to maximize redemptions. The Ritz-Carlton, Dubai International Financial Centre, for instance, cost me just 200,000 Bonvoy points for four nights over New Year’s in 2019, thanks, in part, to the fifth night being free. The same property this year during New Year’s Eve will run more than 400,000 points, a staggering 200% increase in cost.

In my experience, hotel program devaluations are far worse than airline program devaluations.

Currently, Marriott and Hilton offer dynamic pricing for redemptions, while Hyatt has a set award chart with off-peak, standard and peak rates.

Although Hyatt recently shifted hotels within categories for many properties, it isstill a top favorite among TPG staffers and points enthusiasts because of the published award chart. You can redeem a night for as little as 3,500 points (off-peak) or splurge on a Category 8 property for anywhere between 35,000 and 45,000 points a night. The only downside is that its global footprint is not as large as other hotel brands.

Hilton and Marriott are an entirely different story. Due to the sheer number of points required for stays with those brands,saving up points for aspirational stays can take quite some time.

MARRIOTT

I have almost 800,000 Bonvoy points from several years of hotel stays across Marriott brands. Every time I’ve thought of redeeming them, there was either a change in hotel categories or better-priced cash rates that were hard to pass up.

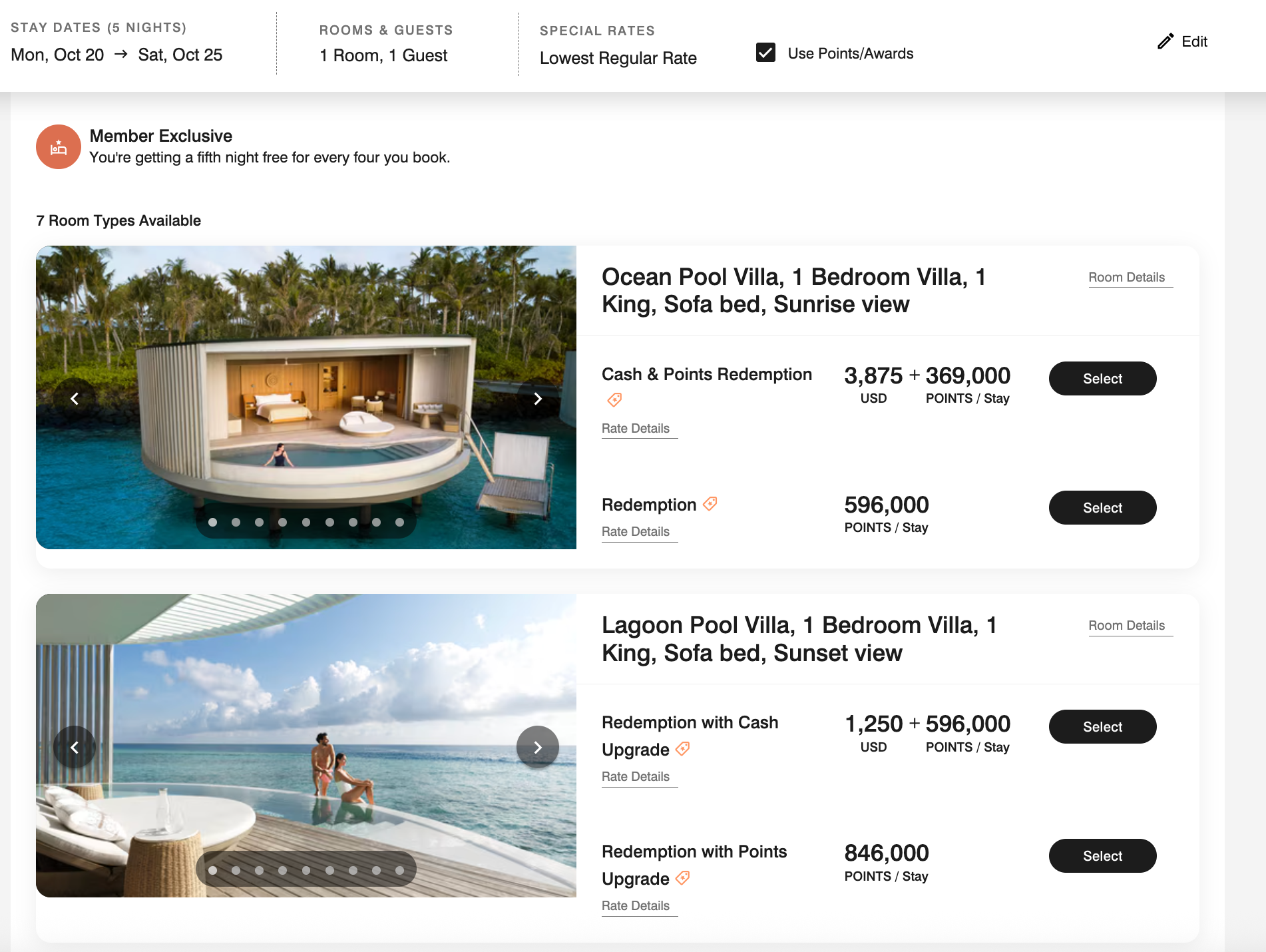

For example, I’ve been eyeing The Ritz-Carlton Maldives, Fari Islands for some time now. A five-night stay in an ocean pool villa would cost 596,000 points, while a similar stay in a lagoon pool villa would set you back 846,000 points. Both options still require a cash copay of over $2,000 for seaplane transfers and some taxes.

The cash rate for the same stay in an ocean pool villa would be $11,675, giving us about 1.95 cents a point in value, almost three times what Marriott points are worth based on TPG’s May 2025 valuations.A lagoon pool villa will set you back $13,206, giving you about 1.56 cents per point in value, according to TPG’s May 2025 valuations. Although these are good deals, it could take a while for Marriott cardholders to amass that many points.

If I had aMarriott Bonvoy Brilliant® American Express® Cardand was trying to collect points solely through hotel spending, I’d have to accrue $28,380 worth of expenses at Marriott properties to make the redemption in the Maldives come to life.I came to that cost based on earning6 points per dollar spent on Marriott purchases and earning an additional 15 points per dollar spent at most properties thanks to having Platinum Elite status.

This would give me enough points for the redemption I’m looking for, but that’s quite a bit of spending (well above what the room would cost cash-wise). Not to mention, you could be hit with another devaluation.

Given how common hotel program devaluations are, I prefer earning transferable rewards versus points with a specific brand through a cobranded hotel card.

My go-to travel credit card is mySapphire Reservebecause it earns 3 points per dollar spent on purchases that code as travel, including hotels. According to TPG’s May 2025 valuations, Chase Ultimate Rewards points are worth 2.05 cents apiece.

Chase Ultimate Rewards points transfer to 11 airline and three hotel programs, giving me flexibility when using my points. I don’t have to worry about Chase points being devalued, and rarely does an issuer sever ties with a transfer partner.

Thanks to my Platinum Elite status, I earn 15 points per dollar spent at most Marriott properties, giving me a 10.5% return on purchases. While that may seem like a lot, keep in mind that according to TPG’s May 2025valuations, Marriott Bonvoy points are worth 0.7 cents apiece, which is about a third of the value of Chase Ultimate Rewards points.

I have other ways to enjoy elitelike perks

The biggest benefit of a cobranded hotel credit card is the ability to have instant elite status or a pathway to earning it.

The information for the Hilton Honors American Express Aspire card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Some would argue that instant top-tier elite status makes a card worth it, but I would argue that the number of elite members with hotel programs makes the most desirable perks like room upgrades tough to come by.

I can use elitelike perks without having a cobranded hotel credit card, thanks to programs such as American Express Fine Hotels + Resorts and The Edit by Chase Travel℠. When booking eligible properties, these programs provide breakfast for up to two guests, room upgrades, property credit, early check-in, late checkout and welcome amenities.

Four Seasons Tokyo at Otemachi. DANYAL AHMED/THE POINTS GUY

Another way I earn elitelike perks is by using specialty travel agencies. These travel agencies are part of unique programs with top brands that offer similar or better perks than Amex Fine Hotels + Resorts and The Edit and predate those programs.

If a travel agency is a Four Seasons Preferred Partner, a Rosewood Elite partner, an Aman partner or affiliated with another similar partner program, then you can expect unique rates, offers and elitelike perks when booking through it.

On a recent trip to Tokyo, I was upgraded to a suite at the Four Seasons Hotel Tokyo at Otemachi, given a property credit of $200 and provided with both early check-in and late checkout. In my experience, these programs are a lot more consistent at providing perks than hotel elite status.

It has been nearly a decade since I began using points and miles, and I am still without a cobranded hotel credit card. My desire to earn transferable points and to have flexibility with the brands I choose to stay at, plus the high points costs for free nights, have kept me from needing one.

Overall, my travel style and increasing interest in seeking out brands without loyalty programs (think: Four Seasons, Mandarin Oriental and Rosewood, among others) are the main drivers for me not getting a hotel credit card. Points-wise, I benefit more from earning transferable points, as I tend to use them to book premium cabin airfare.

Despite not having a hotel credit card, I still earn status with Marriott through paid stays and achieve elitelike benefits through status or booking through special programs with travel agents. Unless there are major negative changes that come to my transferable rewards credit card, I will continue to be without a hotel credit card.

Travelers with plans to stay at an IHG brand and IHG One Rewards loyalists, listen up: You could save hundreds of dollars each year by add...

"Green Horizons Traveler" is your go-to blog for sustainable and eco-friendly travel. We explore the world’s most stunning natural wonders while focusing on responsible tourism. Through inspiring stories, tips, and guides, we help you discover breathtaking destinations that prioritize conservation. Whether hiking through forests or relaxing on pristine beaches, we show you how to travel mindfully and make a positive impact. Join us on a journey to protect our planet while experiencing its beauty.